Semiconductor Leaders' Marketshares Surge Over the Past 10 Years

Top 25 companies held more than three-fourths of worldwide semiconductor market.

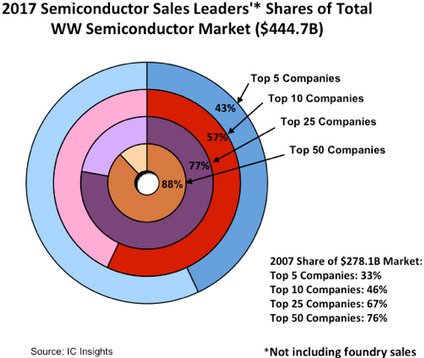

April 11, 2018 -- Research included in the April Update to the 2018 edition of IC Insights’ McClean Report shows that the world’s leading semiconductor suppliers significantly increased their marketshare over the past decade. The top-5 semiconductor suppliers accounted for 43% of the world’s semiconductor sales in 2017, an increase of 10 percentage points from 10 years earlier (Figure 1). In total, the 2017 top-50 suppliers represented 88% of the total $444.7 billion worldwide semiconductor market last year, up 12 percentage points from the 76% share the top 50 companies held in 2007.

Figure 1

As shown, the top 5, top 10, and top 25 companies’ share of the 2017 worldwide semiconductor market each increased from 10-12 percentage points over the past decade. With the surge in mergers and acquisitions expected to continue over the next few years (e.g., Qualcomm and NXP), IC Insights believes that consolidation will raise the shares of the top suppliers to even loftier levels.

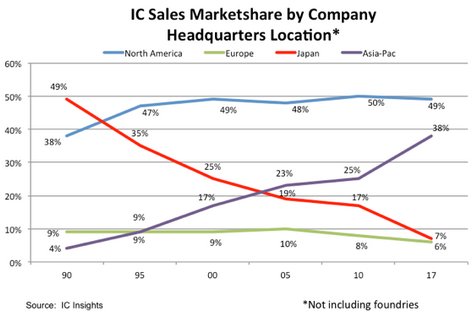

As shown in Figure 2, Japan’s total presence and influence in the IC marketplace has waned significantly since 1990, with its IC marketshare (not including foundries) residing at only 7% in 2017. Once-prominent Japanese names missing from the top IC suppliers list are NEC, Hitachi, Mitsubishi, and Matsushita. Competitive pressures from South Korean IC suppliers—especially in the memory market—have certainly played a significant role in changing the look of the IC marketshare figures over the past 27 years. Moreover, depending on the outcome of the sale of Toshiba’s NAND flash division, the Japanese-companies’ share of the IC market could fall even further from its already low level.

Figure 2

With strong competition reducing the number of Japanese IC suppliers, the loss of its vertically integrated businesses, missing out on supplying ICs for several high-volume end-use applications, and its collective shift toward the fab-lite IC business model, Japan has greatly reduced its investment in new semiconductor wafer fabs and equipment. In fact, Japanese companies accounted for only 5% of total semiconductor industry capital expenditures in 2017 (two points less than the share of the IC market they held last year), a long way from the 51% share of spending they represented in 1990.

Report Details: The 2018 McClean Report

Additional details on sales rankings for the top 50 semiconductor, top 50 IC, and leading IC foundry rankings are provided in the April Update to The McClean Report—A Complete Analysis and Forecast of the Integrated Circuit Industry. A subscription to The McClean Report includes free monthly updates from March through November (including a 250+ page Mid-Year Update), and free access to subscriber-only webinars throughout the year. An individual user license to the 2018 edition of The McClean Report is priced at $4,290 and includes an Internet access password. A multi-user worldwide corporate license is available for $7,290.

Related Semiconductor IP

- UCIe D2D Adapter & PHY Integrated IP

- Low Dropout (LDO) Regulator

- 16-Bit xSPI PSRAM PHY

- MIPI CSI-2 CSE2 Security Module

- ASIL B Compliant MIPI CSI-2 CSE2 Security Module

Related News

- Global Semiconductor Sales Increase 18.8% in Q1 2025 Compared to Q1 2024; March 2025 Sales up 1.8% Month-to-Month

- Global Semiconductor Sales Increase 2.5% Month-to-Month in April

- Intel Appoints Sales and Engineering Leaders

- Global Semiconductor Sales Increase 27.0% Year-to-Year in May

Latest News

- Silicon Creations Celebrates 20 Years of Global Growth and Leadership in 2nm IP Solutions

- TSMC Debuts A13 Technology at 2026 North America Technology Symposium

- Cadence Collaborates with TSMC to Accelerate Design of Next-Generation AI Silicon

- Synopsys Partners with TSMC to Power Next-Generation AI Systems with Silicon Proven IP and Certified EDA Flows

- JEDEC® Previews LPDDR6 Roadmap Expanding LPDDR into Data Centers and Processing-in-Memory