Memory Market Collapse to Lift TSMC to Top Spot in 3Q22 Ranking

Plunge in memory market to drop Samsung to second place; Intel expected to fall to third.

September 08, 2022 -- In its August Quarterly Update to The McClean Report released last month, IC Insights reduced its worldwide IC market growth forecast for 2022 from 11% to 7%. The downgraded expectation for this year is almost entirely due to the collapse of the memory market in the second half of 2022. As discussed below, it was as though someone “flipped a switch” to the off position for the memory market beginning in June!

The few memory companies that have made statements about the recent developments in the memory market have attributed the swift downturn to a massive inventory adjustment currently underway by their customers. Moreover, most expect this inventory adjustment period to extend into at least early 2023.

The following statements and data from a few of the memory suppliers yield some insight into how fast the market has changed over the past couple of months.

• When Micron’s fiscal 3Q ended in May, the company gave an early warning of the trouble that was brewing in the memory market. Although the company’s fiscal 3Q sales were solid, it presented 4Q (ending in August) sales guidance of -17%. Moreover, Micron revised this figure to at least a 21% drop in sales for its fiscal quarter that ended in August.

• In its 2Q conference call, major NAND flash memory supplier Western Digital commented that the inventory adjustment currently underway is “definitely very, very sharp in the quarter we are in (3Q22).” Western Digital’s outlook is for a company-wide sales decline of 18% this quarter. With hard disk drives (HDDs) making up about half of the company’s sales and expected to show only a modest decline in 3Q, IC Insights believes that its NAND flash business is likely to register a drop of at least 20% this quarter.

• In early September, Kyung Kye-hyun, Samsung’s co-CEO and head of its semiconductor unit said, “The second half of this year looks bad, and as of now, next year doesn’t really seem to show a clear momentum for much improvement.”

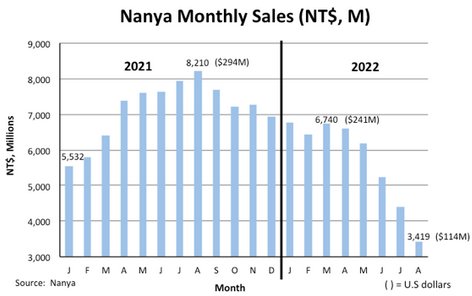

• Taiwan-based Nanya is a relatively minor player in the global DRAM market, but its monthly sales data provides some insight into how swiftly the DRAM market can shift gears from boom to bust. As shown in Figure 1, the company’s August 2022 DRAM sales, when shown in U.S. dollars, were 39% of what they were in August 2021 and down 53% from March’s sales, just five months ago!

Figure 1

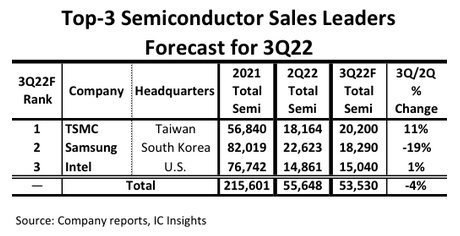

With the memory market currently in a free-fall, IC Insights expects foundry giant TSMC to surpass Samsung and take over the top spot in the semiconductor company sales ranking in 3Q22 (Figure 2). As shown, Intel is expected to move to the third position in the ranking with 3Q22 sales that are 26% less than TSMC’s. Illustrating the swiftness of TSMC’s rise to the top, TSMC was ranked as the third largest semiconductor supplier in the world in 2021 and had sales that were 31% less than Samsung’s.

The sheer magnitude of TSMC’s semiconductor sales comes more into focus when one considers the “final” sales of company. The “final” sales figure for a pure-play foundry like TSMC is about 2x the total foundry sales number. The 2x multiplier estimates the semiconductor sales amount sold to the final customer (i.e., the electronic system producer). For example, fabless company AMD purchases processors from TSMC but AMD is not the final end-user of these devices. AMD resells these processors to electronic system producers at a much higher price than it paid TSMC for the parts. As a result, a 2x multiplier, which assumes a 50% gross margin for the foundry’s customers (e.g., AMD), can be used to arrive at a “final” semiconductor market sales figure for TSMC.

Figure 2

Using a “final” sales figure estimate for TSMC puts its 2021 semiconductor sales at $113.7 billion and $40.4 billion for 3Q22! To put the company’s “final” 2021 semiconductor sales figure into perspective, at $113.7 billion, TSMC’s “final” sales are estimated to have represented 18.5% of the world’s semiconductor market last year. Moreover, IC Insights believes that this percentage has a good chance of rising to 25% in 3Q22.

Report Details: The 2022 McClean Report

The McClean Report—A Complete Analysis and Forecast of the Semiconductor Industry, is now available. A subscription to The McClean Report service includes the January Semiconductor Industry Flash Report, which provides clients with IC Insights’ initial overview and forecast of the semiconductor industry for this year through 2026. In addition, the third of four Quarterly Updates to the report was released in August, with one additional Quarterly Update to be released in November of this year. An individual user license to the 2022 edition of The McClean Report is available for $5,390 and a multi-user worldwide corporate license is available for $8,590. The Internet access password and the information accessible to download will be available through November 2022.

https://www.icinsights.com/services/mcclean-report/pricing-order-forms/

Related Semiconductor IP

- Zigbee Transceiver PHY

- Data Flow Architecture IP

- AMBA SPI Controller MRAM Controller

- Ethernet MAC

- Protocol Bridges

Related News

- Total Revenue of Global Top 10 IC Design Houses for 3Q22 Showed QoQ Drop of 5.3%; Broadcom Returned to No. 2 Spot in Revenue Ranking by Overtaking NVIDIA and AMD, Says TrendForce

- Strong AI Demand and Early Consumer Electronics Inventory Build Drive Top 10 Foundries to 3.7% QoQ Revenue Growth in 1Q26

- Imec achieves breakthroughs in ferroelectric memory research for next-generation memory solutions to meet AI-era data needs

- New iPhone Models Become Key to Qualcomm's Top Spot in 3Q20 Revenue Ranking of Global Top 10 IC Design (Fabless) Companies, Says TrendForce