AI Component Capacity Squeeze and Foundry Output Cuts to Extend Mature-Node Price Increases in 2027

June 30, 2026 -- TrendForce’s latest research reveals that rising demand for AI servers, general-purpose servers, and edge AI devices is prompting foundries to dedicate an increasing share of wafer capacity to AI-related products. This shift has significantly altered the supply-and-demand balance for mature process nodes.

On the 8-inch side, rising demand for AI power devices, together with production cuts by TSMC and Samsung, has driven both capacity utilization and foundry prices sharply higher.

In the 12-inch mature-node segment, TSMC's production cuts are expected to create mid- to long-term order transfer opportunities. At the same time, strong demand for power ICs on 55nm and larger nodes has tightened the high-voltage (HV) process capacity at Taiwanese foundries, prompting some HV orders to shift to Chinese suppliers. These developments—combined with incremental AI-driven demand and raw material inflation—are strengthening pricing momentum for 12-inch mature-node foundry services.

TrendForce expects this upward pricing trend to extend through to 2027.

TrendForce notes that, in recent years, leading foundries have steadily reduced 8-inch and 12-inch mature-node capacity in favor of advanced process technologies and advanced packaging. Second- and third-tier foundries are also reallocating limited capacity toward higher-margin AI-related applications, including PMICs, power discrete devices, interposers, DTC/IPD/IPC, PICs, and optical communication TIAs, while scaling back production of lower-margin products such as CIS and DDICs.

The first wave of full utilization has already emerged at Chinese 8-inch foundries, with Taiwanese and Korean manufacturers subsequently entering increasingly tight supply conditions, particularly for power-device production lines. TrendForce data shows that average utilization across the world's top ten foundries' 8-inch fabs recovered to 88% in 2026 and is expected to reach 90% in the second half of the year, indicating that supply for 8-inch mature-node capacity has already become constrained.

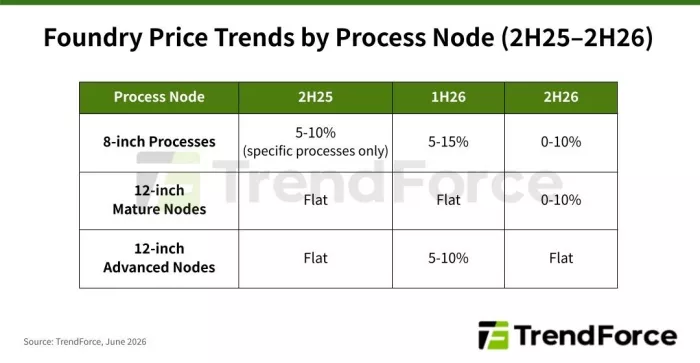

Utilization rates have tightened significantly since PMICs and power discrete devices remain highly dependent on 8-inch manufacturing platforms, and major foundries such as TSMC and Samsung continue to reduce or repurpose 8-inch capacity. Foundry prices have risen across the board between the first and second quarters of 2026, with average increases ranging from 5% to 15%. The industry is also preparing a third round of price increases that could extend from the second half of 2026 into 2027.

For 12-inch mature processes, AI-driven demand is increasing wafer consumption for 55nm-and-above power devices, 65/55nm silicon interposers, and 40/28nm FPGAs. Over the longer term, TSMC's consolidation and reduction of mature-node capacity—together with order reallocation following PSMC's divestment of its P5 fab—are expected to reshape market dynamics.

Meanwhile, emerging applications, including silicon bridges/interposers, DTC/IPD, PICs, NAND Flash CMOS, and HBF driver/base dies, are steadily occupying additional capacity, extending visibility for 12-inch mature-node utilization well into 2027.

Although foundries continue expanding 12-inch mature-node capacity, new investments are increasingly directed toward higher-margin products. This is squeezing capacity allocated to lower-margin HV and CIS manufacturing. To ensure a stable supply while maintaining pricing flexibility, customers are increasingly turning to Chinese foundries as alternative manufacturing partners, driving additional order growth for China's mature-node ecosystem.

Overall, the 12-inch mature-node market has gradually recovered from the weakness seen over the past several quarters. However, rising raw material costs are placing additional pressure on foundries' manufacturing expenses. Prices for several capacity-constrained process nodes have already begun to show signs of increasing by 5–10% between the second and third quarters of 2026, with suppliers aiming for broader price hikes in 2027.

On the demand side, however, rising memory prices and increasing costs for other electronic components are expected to weigh on consumer electronics shipments during the second half of the year. As a result, many customers are negotiating to postpone planned foundry price increases scheduled for the second half of 2026. Nevertheless, inflation in semiconductor manufacturing materials, continued capacity reductions by major foundries, and sustained capacity consumption from emerging AI applications suggest that further mature-node price increases in 2027 are likely to be difficult to avoid.

For more information on TrendForce’s semiconductor reports and market data, please visit the Report Page, leave a Message, or Email (SR_MI@trendforce.com) the Sales Department.

Related Semiconductor IP

- Zigbee Transceiver PHY

- Data Flow Architecture IP

- AMBA SPI Controller MRAM Controller

- Ethernet MAC

- Protocol Bridges

Related News

- 2H25 Foundry Utilization Exceeds Expectations, Some Players Are Prepared for Price Hikesorce

- Eliyan Ports Industry’s Highest Performing PHY to Samsung Foundry SF4X Process Node, Achieving up to 40 Gbps Bandwidth at Unprecedented Power Levels with UCIe-Compliant Chiplet Interconnect Technology

- DDR4 and LPDDR4 Supply Tightens Sharply in 2H25 as Structural Shortage Drives Strong Price Surge, Says TrendForce

- Unlock seamless video transmission between graphics adapters and LCD displays with readily licensable, silicon-proven LVDS IP cores tailored for the advanced 22FDX process node