2024 Global Fab Equipment Spending Recovery Expected After 2023 Slowdown, SEMI Reports

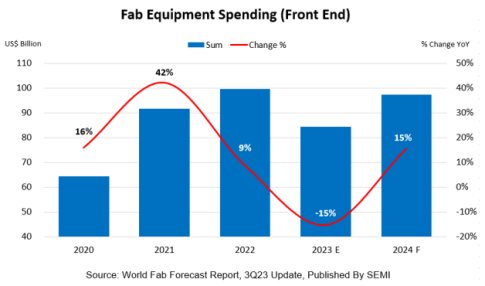

MILPITAS, Calif. — September 12, 2023 — Global fab equipment spending for front-end facilities in 2023 is expected to decline 15% year-over-year (YoY) to US$84 billion from a record high of US$99.5 billion in 2022 before rebounding 15% YoY to US$97 billion in 2024, SEMI announced today in its latest quarterly World Fab Forecast report. Softening chip demand and elevated inventory of consumer and mobile devices will contribute to the 2023 decline.

Next year’s fab equipment spending recovery will be partly driven by the end of the semiconductor inventory correction in 2023 and strengthening demand for semiconductors in the high-performance computing (HPC) and memory segments.

“The 2023 decline in equipment investment is proving shallower and the 2024 rebound stronger than expected earlier this year,” said Ajit Manocha, SEMI president and CEO. “The trend suggests the semiconductor industry is turning the corner on the downturn and on a path back to robust growth fueled by healthy chip demand.”

Foundry Segment Continues to Lead Semiconductor Industry Expansion

The foundry segment is expected to lead the semiconductor expansion in 2023 with US$49 billion in investments, 1% growth, and US$51.5 billion in spending in 2024, a 5% increase as investment continues in leading-edge and mature process nodes. Memory spending is forecast to stage a strong comeback in 2024 with a 65% increase to US$27 billion after a 46% decline in 2023. Specifically, DRAM investments are expected to decline 19% YoY to US$11 billion in 2023 but recover to US$15 billion, a 40% annual jump, in 2024. NAND spending is projected to mirror that trend, decreasing 67% to US$6 billion in 2023 but surging 113% to US$12.1 billion in 2024. MPU investments are expected to remain flat in 2023 and increase 16% to US$9 billion in 2024.

Taiwan Continues to Lead Equipment Spending

Taiwan is expected to retain the global lead in fab equipment spending in 2024 with US$23 billion in investments, a 4% YoY increase. Korea is projected to rank second in spending, with an estimated US$22 billion in investments in 2024, a 41% jump from this year reflecting a memory sector recovery. With export controls expected to limit China’s spending in leading-edge technologies and foreign investment, the region is forecast to place third in equipment spending worldwide in 2024 at US$20 billion, a decline from 2023 levels. Despite the constraints, Chinese foundry suppliers and IDMs are expected to continue investments in mature process nodes.

The Americas is expected to remain the fourth largest region in spending, reaching a historic high of US$14 billion in investments in 2024, a 23% YoY increase. The Europe and Mideast region is also forecast to log record investments next year, increasing spending by 41.5% to US$8 billion. Fab equipment spending in Japan and Southeast Asia is expected to increase to US$7 billion and US$3 billion, respectively, in 2024.

Covering 2022 to 2024, the SEMI World Fab Forecast report shows the global semiconductor industry increasing capacity by 5% this year after an 8% rise in 2022. Capacity growth is expected to continue in 2024, climbing 6%.

The latest update of the SEMI World Fab Forecast report, published in September, lists 1,477 facilities and lines globally, including 169 facilities and lines with various probabilities expected to start operation in 2023 or later.

Download a sample of the SEMI World Fab Forecast report.

For details about SEMI reports on other semiconductor sectors, visit SEMI Market Data or contact the SEMI Market Intelligence Team (MIT) at mktstats@semi.org.

About SEMI

SEMI® connects 3,000 member companies and 1.3 million professionals worldwide to advance the technology and business of electronics design and manufacturing. SEMI members are responsible for the innovations in materials, design, equipment, software, devices, and services that enable smarter, faster, more powerful, and more affordable electronic products. Electronic System Design Alliance (ESD Alliance), FlexTech, the Fab Owners Alliance (FOA), the MEMS & Sensors Industry Group (MSIG) and SOI Consortium are SEMI Strategic Technology Communities. Visit www.semi.org to learn more.

Related Semiconductor IP

- UCIe D2D Adapter & PHY Integrated IP

- Low Dropout (LDO) Regulator

- 16-Bit xSPI PSRAM PHY

- ASIL B Compliant MIPI CSI-2 CSE2 Security Module

- SHA-256 Secure Hash Algorithm IP Core

Related News

- Global Fab Equipment Spending on Track for 2024 Recovery After 2023 Slowdown, SEMI Reports

- SEMI Projects Double-Digit Growth in Global 300mm Fab Equipment Spending for 2026 and 2027

- Fab Equipment Spending Breaking Industry Records

- Total Fab Equipment Spending Reverses Course, Growth Outlook Revised Downward

Latest News

- TSMC Chases Soaring AI Demand

- EU DARE Project Is Scrambling to Replace Codasip

- Sofics and Alcyon Photonics Partner to Support Next-Generation Photonic Systems

- QuickLogic Appoints Quantum Leap Solutions as Authorized Sales Representative

- Cadence and NVIDIA Expand Partnership to Reinvent Engineering for the Age of AI and Accelerated Computing