AI Demand Drives 4Q25 Global Top 10 Foundries Revenue Up 2.6% QoQ; Samsung Gains Share and Tower Moves Up in Rankings

March 12, 2026 -- TrendForce’s latest research on the semiconductor foundry industry reveals that advanced-node demand remained strong in 4Q25, driven by the tight supply of AI server GPUs and Google TPUs. Furthermore, the launch of new smartphones boosted wafer orders for mobile application processors (APs), supporting solid shipment performance.

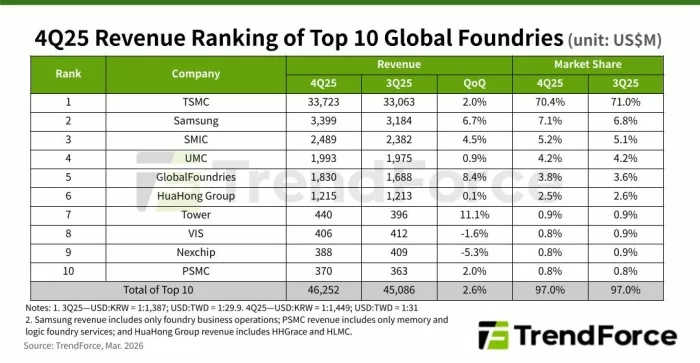

On the mature-node side, PMIC orders related to servers and edge AI continued to keep 8-inch fabs running at high utilization rates, with some suppliers even considering price increases. Meanwhile, utilization rates at 12-inch fabs remained largely stable. Together, these factors pushed the combined revenue of the world’s top ten foundries up 2.6% QoQ to nearly US$46.3 billion in 4Q25.

The leading ten foundries achieved around $169.5 billion in revenue in 2025, a 26.3% YoY increase that set a new industry record. Looking ahead to 2026, initial inventory build-up for some consumer products might help stabilize utilization rates early in the year. However, rising memory prices are anticipated to dampen demand for mainstream end devices, leading to uncertainty in orders and fab utilization in the latter half of the year.

Among major foundries, TSMC saw slightly lower wafer shipments in 4Q25, but shipments of new flagship smartphone APs—led by chips for the iPhone 17 series—boosted demand for its 3 nm node. The resulting increase in ASPs lifted quarterly revenue 2% QoQ to $33.7 billion, which allowed TSMC to maintain its leading position with a 70.4% market share.

Samsung Foundry (excluding System LSI) recorded 6.7% QoQ revenue growth to reach nearly $3.4 billion in 4Q25. Revenue was supported by shipments of new 2nm products, as well as the production of logic dies used in Samsung’s HBM4 memory. These contributions helped offset a slight decline in overall fab utilization. Samsung not only returned to profitability but also increased its market share from 6.8% to 7.1% to maintain second place.

SMIC ranked third as the company continued to benefit from localization demand. Revenue rose 4.5% QoQ to almost $2.49 billion, with growth driven by higher wafer shipments, slightly improved ASP, and additional photomask shipments toward the end of the year.

UMC remained fourth, as stable orders from major customers supported both 8-inch and 12-inch fabs. Utilization rates held steady compared with the previous quarter, and revenue increased 0.9% QoQ to around $2 billion.

GlobalFoundries ranked fifth as it benefited from increased demand for data center peripheral components. Both wafer shipments and ASP improved, driving 8.4% QoQ revenue growth to $1.8 billion.

HuaHong Group ranked sixth. At its subsidiary HHGrace, demand for MCUs and PMICs lifted revenue 3.9% QoQ in 4Q25. After consolidating revenue from HLMC, HuaHong Group reported total revenue of approximately $1.22 billion, up 0.1% QoQ.

It’s worth noting that shipments related to emerging server applications such as silicon photonics (SiPho) and silicon-germanium (SiGe) grew steadily in 4Q25. This momentum helped Tower’s semiconductor revenue rise 11.1% QoQ to $440 million, pushing the company ahead of Vanguard and Nexchip to take seventh place.

Vanguard ranked eighth, with revenue declining 1.6% QoQ to $406 million. Shipments were affected by softer demand for DDIC orders and cross-fab qualification issues related to a major PMIC customer.

Nexchip claimed the ninth position, reporting a 5.3% QoQ drop in revenue to $388 million. The decline reflected the company’s decision to delay shipments of certain products to 1Q26 after meeting its 2025 shipment and revenue targets.

Finally, PSMC finished in tenth place. Strong demand for memory foundry services, combined with rising ASPs, lifted quarterly revenue 2% QoQ to approximately $370 million, while its logic foundry business remained relatively stable.

For more information on reports and market data from TrendForce’s Department of Semiconductor Research, please click here, or email the Sales Department at SR_MI@trendforce.com

Related Semiconductor IP

- UCIe D2D Adapter & PHY Integrated IP

- Low Dropout (LDO) Regulator

- 16-Bit xSPI PSRAM PHY

- MIPI CSI-2 CSE2 Security Module

- ASIL B Compliant MIPI CSI-2 CSE2 Security Module

Related News

- Global Top 10 Foundries Q4 Revenue Up 7.9%, Annual Total Hits US$111.54 Billion in 2023, Says TrendForce

- 4Q24 Global Top 10 Foundries Set New Revenue Record, TSMC Leads in Advanced Process Nodes, Says TrendForce

- Total Revenue of Top 10 Foundries Fell by 4.7% QoQ for 4Q22 and Will Slide Further for 1Q23, Says TrendForce

- Top 10 Foundries Report Nearly 20% QoQ Revenue Decline in 1Q23, Continued Slide Expected in Q2, Says TrendForce

Latest News

- Wind River Joins the CHERI Alliance and Collaborates with Innovate UK to Accelerate Cybersecurity Innovation

- Arteris and MIPS Partner to Accelerate Development for Physical AI Platforms

- DCD-SEMI expands CryptOne with EdDSA Curve25519 IP core for secure embedded systems

- Syntacore's SCR RISC-V IP Now Supports Zephyr 4.3

- Xylon Presents New 12-Channel GMSL3/GMSL2 FMC+ ExpansionBoard